Corrado Cominotto, Head of Active Asset Management at Banca Generali

Corrado Cominotto, Head of Active Asset Management at Banca Generali

We are leaving behind a complex 2022 for the bond market, but the macroeconomic environment for 2023 looks more favourable.

2022 was a very complicated year for the financial markets. The negative returns recorded by both equities and bonds were mainly due to the war conflict in Ukraine, which exacerbated the generalised rise in commodity prices already underway after the post-pandemic reopening, generating further inflationary pressures.

This happened in the United States, where the rise in consumer prices peaked at just over 9%. But it also happened in Europe, where inflation exceeded the 10% threshold.

To counter such high price increases, central banks raised their key interest rates several times during the year. The US Federal Reserve raised them by 375 basis points (3.75%) and the European Central Bank by 250 basis points (2.5%). "This context has caused abnormal market movements," says Corrado Cominotto, Head of Asset Management at Banca Generali, "suffice it to say that, over the past 90 years, the stock and bond markets have recorded simultaneous negative performances in only four occasions (1931, 1941, 2018, 2022) and only this year they have both recorded double-digit losses."

During 2022, as Cominotto recalls, capital losses on Eurozone government bonds were in the order of about 14%. In particular, the yield of the German ten-year Bund rose from -0.17% to around 2.2%, while that of the US Treasury from 1.5% to around 3.5%. The restrictive monetary policy implemented by the two governors on both sides of the ocean, Jerome Powell in America and Christine Lagarde in Europe, contributed to a contraction of global gross domestic product growth estimates. And it has increased the probability that economists attribute to the arrival of a recession in the coming year. "The latter seems to be currently priced in by the market," continues Cominotto, who adds: "in both Europe and the US, we are in fact seeing inverted yield curves with short-term government bonds showing higher yields than those on the medium long-term side."

In the bond segment, Italian Btp again had a moment this year, in the aftermath of the Draghi government crisis and the ensuing elections, when there was an increase in the spread (i.e. the yield differentials) of ten-year Treasury bonds compared to German Bunds of the same duration. To be more precise, the spread on ten-year bonds reached 250 basis points (to then fall back to around 210 basis points to date). "Such market stresses on Italian government bonds are not new and have already occurred several times in recent years," recalls Banca Generali's Head of Active Asset Management. In addition to the 10-year maturity, the widening has also affected short maturities, with the yield differential on 2-year BTP-Bund government bonds reaching 130 basis points, only to retrace, to date, to a much more modest level of 65 basis points. During the most stressful phases, however, the European Central Bank intervened verbally, reminding us that there are instruments to maintain the stability of Eurozone members' spreads.

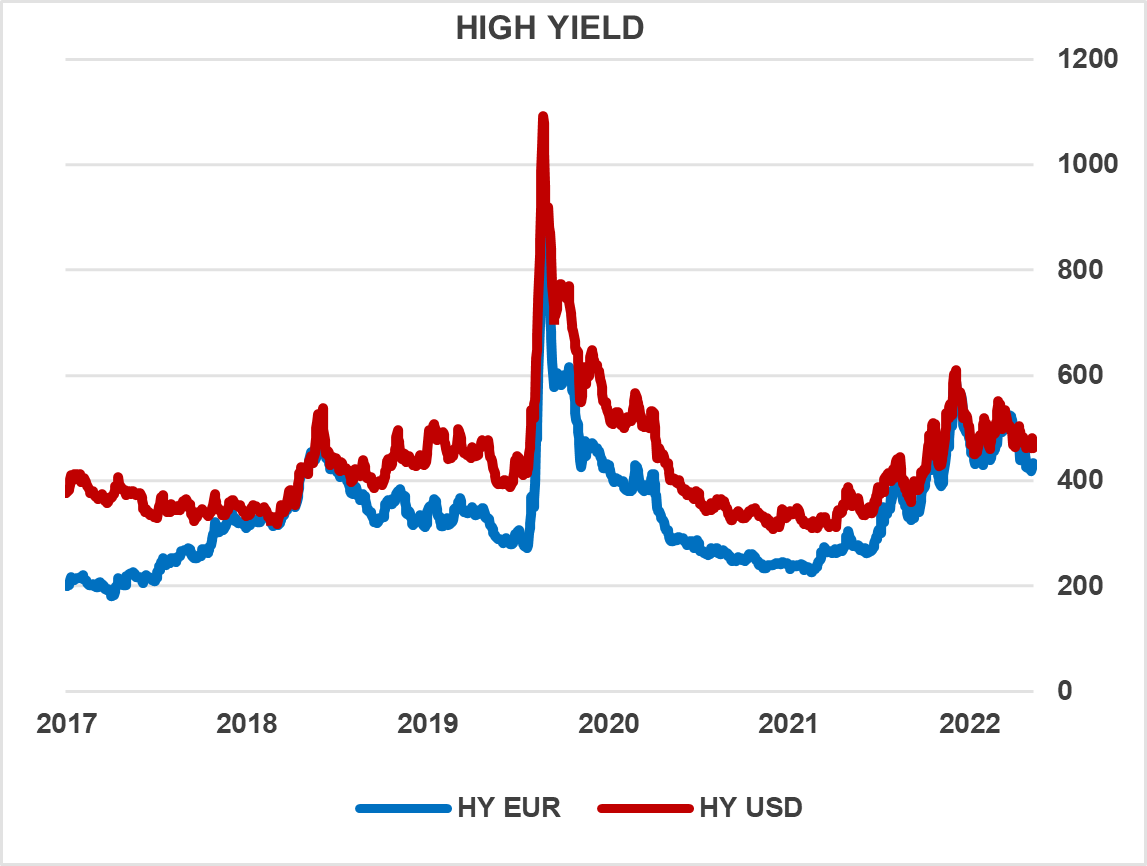

On the corporate bond front (debt securities issued by private companies) credit spreads widened in the course of 2022 for both Investment Grade (i.e. rated above triple B) and High Yield (rated below triple B) bonds. The latter, more than the Investment Grade spreads, only partially recovered in the last quarter of the year thanks to the lower-than-expected inflation data in the US. "Currently, the level of yields in the High Yield segment is such that coupons offer good protection should spreads widen again in the coming weeks", says Cominotto.

Internal source

Lastly, Banca Generali's Head of Active Asset Management points out that, "after several years of near-zero and in many cases even negative yields, the macroeconomic environment for 2023 looks more favourable for bond investments than in the past. This view is a consequence of a central bank approach that is expected to be less aggressive in 2023 and tends to end the cycle of rate hikes. The current yields, between 2% and 8% depending on the risk profile of the issue, pre-date a realistic scenario compared to current forecasts". For Cominotto, it should also be taken into account that many of the companies in the market have locked up their debt in the past years and will have to refinance themselves in the market mostly from 2024 onwards. This should allow default rates (i.e. non-repayment at maturity of securities) not to increase too significantly in the coming year.

Corrado Cominotto, Head of Active Asset Management at Banca Generali

We are leaving behind a complex 2022 for the bond market, but the macroeconomic environment for 2023 looks more favourable.

/original/BLOG+-+BANNER+%288%29.png)