13 October 2022#WeeklyWatch

Rating agencies and warnings to governments: why?

First Moody's and then Fitch. These are the two famous U.S. agencies that have issued warnings to Italy in recent weeks as the new legislature begins.

Both have not ruled out revising the rating on our country downward if there is a deterioration in the economic picture and if the new government's fiscal policies are not rigorous enough and the reform agenda related to the NRP is changed substantially.

On closer inspection, our country is not the only one that has received a warning from rating agencies. On the contrary, in previous weeks, Britain in particular had come into the crosshairs, which, after the maneuver based on tax cuts and debt increases decided by the government in London, had lowered the outlook on the UK from stable to negative, while provisionally keeping its rating unchanged.

Fitch did the same thing last week, again looking at the trans-Atlantic government's maneuvering and its loose fiscal policies. But why is the rating agencies' judgment so important and what is it for?

Rating agencies: what are they?

To understand this, one must first know what rating agencies are. They are independent companies that assign a judgment regarding the financial strength and reliability of an entity issuing bonds on a regulated market.

The largest is the U.S.-based Standard & Poor's, followed by compatriots Moody's and Fitch. Fourth player in the market (albeit spaced out) is the Toronto-based Dbrs Group. Agency ratings are especially important in assessing the reliability as a debtor of an entity (whether it is a corporation, a sovereign entity, or an actual state).

A debtor with a high rating is considered safer. And securities that the same debtor issues in the market are also judged safer.

Specifically, these are bonds, securities through which a company can finance itself by borrowing money from investors, with the promise to return it at a specified maturity, subject to the payment, at defined intervals, of certain interest. When it is a sovereign nation that issues the bond, on the other hand, you have a government bond (which in Italy is called a "Buono del Tesoro").

Rating agencies: what are they for?

To assess the financial reliability of issuers/states, rating agencies "sift" through the issuers'/governments' balance sheet/budget, making positive or negative judgments on the choices made on corporate governance/deficit and making predictions on how debt levels will evolve in the years to come.

In particular, the judgment of a rating agency on sovereign countries, such as Italy, Great Britain or any other industrialized nation that issues bonds in the financial market, assumes important relevance, and that is why it is readily taken up in the financial news, representing a compass that investors have at their disposal to orient themselves and choose whether or not to buy a debt security of those countries.

How do they work?

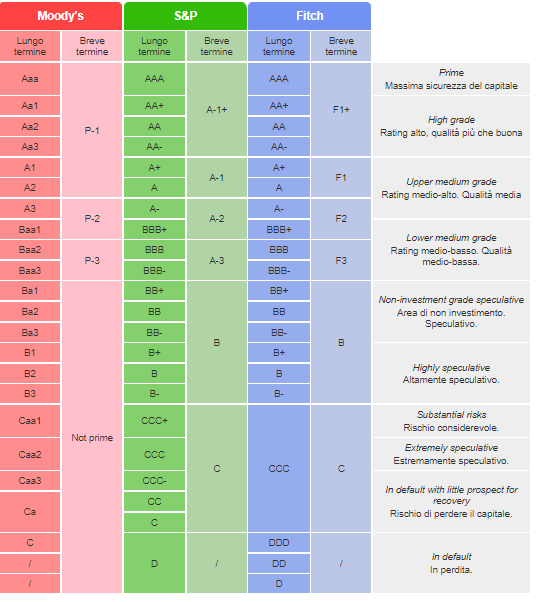

Agency ratings are expressed through the letters of the alphabet. Each letter or series of letters corresponds to a certain score. Each agency has its own scale, although the methodology used is comparable with the others.

S&P and Fitch use a system of capital letters ranging from A to D. Triple A (AAA) corresponds to the highest score and indicates higher financial reliability of the issuer. Single D corresponds to the lowest score (default). So, if a state is given a triple-A rating, the bonds it issues are considered by investors to be more reliable.

Moody's uses a slightly different rating scale than the other two agencies (it alternates capital and lowercase alphabet letters from A to C, also accompanied by numbers). Moody's rating system, however, does not differ much from that of S&P and Fitch. In fact, in all cases, the rating scale used by the agencies has a downward trend: each step indicates a gradually less positive judgment of the borrower's creditworthiness.

Currently, S&P assigns Germany a triple-A rating, given the country's low debt and higher financial strength than, for example, Italy, which S&P assigns a triple-B rating given its higher level of government debt. Lower credit quality corresponds to a higher yield demanded by investors, which partly explains the yield difference between a BUND and a BTP.

In addition to assigning a score expressed in letters, when they update their ratings on an issuer/state, the agencies also indicate the "outlook," i.e., the outlook on the issuer's/state's creditworthiness for the following months. A negative outlook projects a deteriorating debtor's creditworthiness, while a positive outlook projects the exact opposite, i.e., an improvement in the issuer's financial situation and an improved ability to honor its debts.

The rating assigned to an issuer may change over time. When agencies consider whether or not to change it, they first place the issuer/state under observation, making the news public. They also declare the start of the rating review process by updating the outlook, positively in case the observation is for a possible upward revision of the rating (upgrade), negatively if there is a possibility of a possible downgrade.

Usually the rating review action takes quite a long time, more than six months. In exceptional situations, it is possible, however, for rating agencies to issue a Credit Watch warning on an issuer, signaling the need to re-evaluate its rating in a shorter time frame upon the occurrence of contingent factors that may impact the credit rating.

In addition, agencies assign a rating not only to issuers but also to individual issues, i.e., bonds issued. In this case, in addition to providing an overall assessment of the issuer's creditworthiness, the agency evaluates specific aspects and characteristics of the bond (including the type of coupon, maturity, etc...) to assess, for example, the issuer's ability to repay principal and interest, on the bond's maturity date. In the latter case, for example, the agency assesses the maturity concentration of the issuer's debt and the resulting solvency over time.