Generoso Perrotta, Head of Financial Advisory

Generoso Perrotta, Head of Financial Advisory

Overweight position on the bond asset class and neutral stance on the equity asset class, always ready to seize opportunities that arise in the coming months.

A perfect storm. This is what investors had to face in 2022, a year that will be remembered by them as 'miserable' and during which both the stock and bond markets simultaneously recorded double-digit losses.

Sharply rising inflation globally, the resulting restrictive monetary policies of the major central banks, slowing global economic growth, the war in Ukraine, the energy crisis in Europe and the slowdown in economic activity in China due to Covid-related restrictions were the triggers that overlapped unexpectedly, creating a spiral that left investors with no chance of sheltering in a safe haven and achieving positive returns.

Bond market performance: Barclays Global Aggregate

"In a context so complex and volatile as the one we have just experienced," comments Generoso Perrotta, Head of Financial Advisory at Banca Generali, "an adequate diversification of portfolios, through a structured strategic approach, is the tool needed to rebuild assets affected by such a negative 2022."

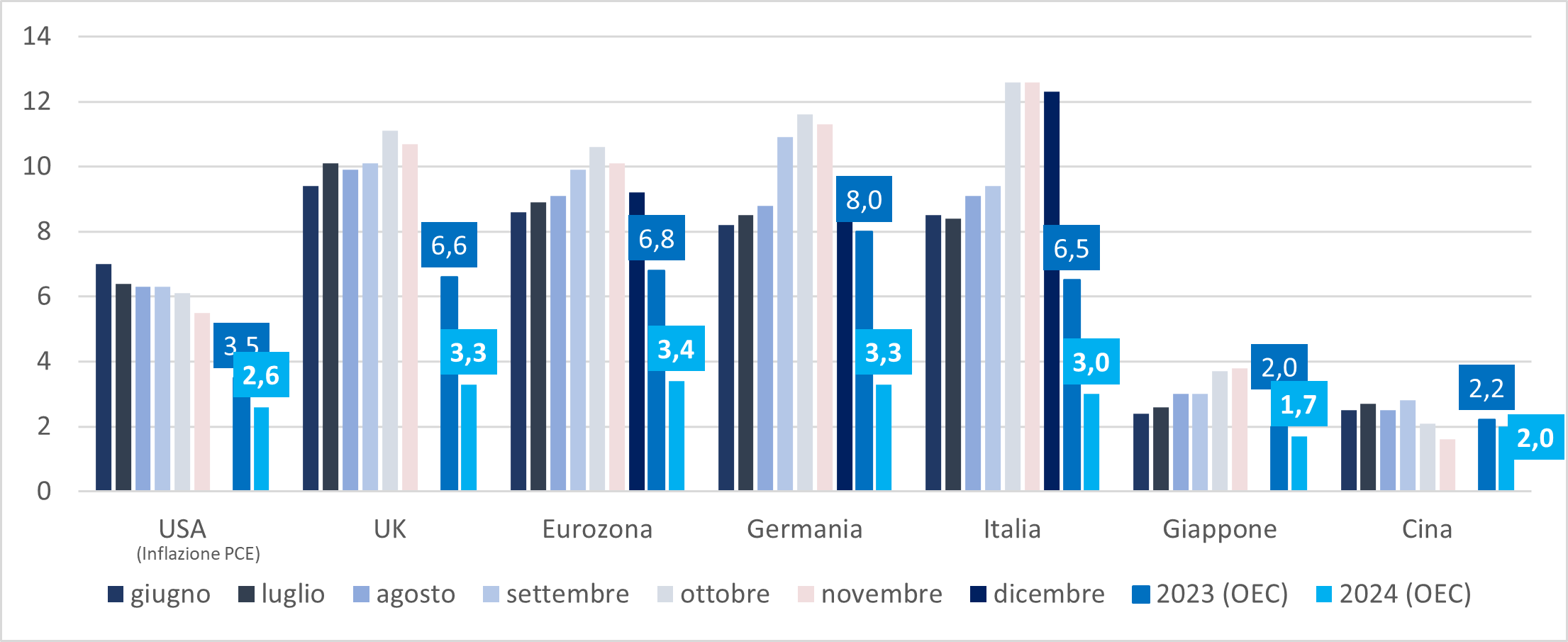

Some of the factors that adversely affected equity markets in 2022 seem set to gradually fade away: inflation has provided the first signs of a slowdown in both the US and the Eurozone; the Fed and the Bce, although still determined to maintain a restrictive approach, have moderated the intensity of their latest rate hikes and China has lifted restrictions on mobility in the country, with predictable positive effects on economic growth.

However, it cannot be taken for granted that a bullish phase will emerge soon.

"For stock prices to experience a more solid and lasting rebound," adds Perrotta, "confirmation will be needed on whether inflation is actually returning to target and on the resilience of the major economies, which as of today still appear set to suffer from monetary tightening and the energy crisis". Indeed, Banca Generali's Head of Financial Advisory points out that the price level is still high and the central banks have not yet finished their work: there is a risk that excessively restrictive monetary policies could have more serious and persistent effects on economic growth than expected, with consequences on corporate profits that have not yet been discounted by the market. "It is therefore necessary to monitor the situation carefully, without giving in to either fear or enthusiasm," adds Perrotta, "thus advising a prudent approach, oriented towards a neutral positioning on the equity asset class, keeping ready to seize the opportunities that will arise in the coming months".

Inflation trends in the main countries and economic areas (11.01.2023)

The outlook is different for bond markets, where yields are expected to continue to fall as the restrictive monetary interventions already in place show their full effect in calming the rise in prices, allowing central banks to become progressively less aggressive. "Bond investment therefore appears increasingly attractive thanks also to a particularly attractive level of yields on offer," continues Perrotta, who prefers an overweight positioning on the bond asset class, identifying the most interesting components in the various sovereign countries and in the most financially solid corporate issuers.

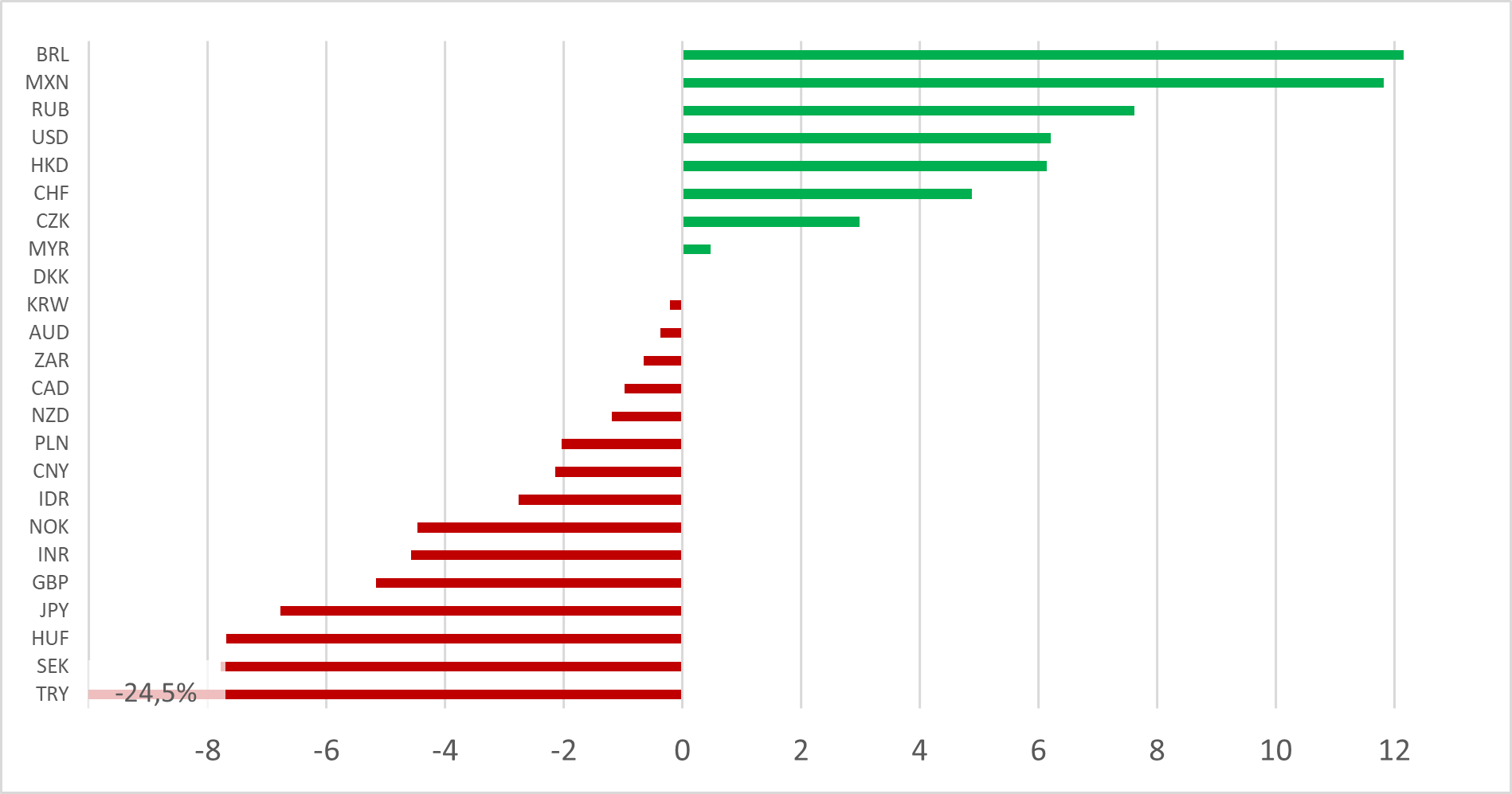

As in the past year, currency diversification will also play a key role in asset allocation choices in 2023.

Looking ahead, it is reasonable to expect the US dollar to gradually depreciate against the euro. Inflation in the Eurozone is still persistent and higher than in the US, so the Federal Reserve could reach the peak in the rate hike path before the ECB. This would lead to a divergence, although temporary, in the monetary policies undertaken by the two institutions: the Fed pausing and the Bce still tightening.

"In this scenario," concludes Banca Generali's Head of Financial Advisory, "the US dollar would be disadvantaged and it would be advisable to gradually reduce its exposure in favour of currencies that have depreciated over the course of 2022 and which could regain ground in the future. For example, the Japanese yen could see its fortunes rise if the Bank of Japan also shows itself willing to change its accommodative monetary policy approach, on the strength of a domestic economy that has been more resilient than others, thanks in part to the weakness of the domestic currency over the past year".

Performance of major currencies vs. EUR in 2022

Generoso Perrotta, Head of Financial Advisory

Overweight position on the bond asset class and neutral stance on the equity asset class, always ready to seize opportunities that arise in the coming months.

/original/BLOG+-+BANNER+%288%29.png)