"Recent economic data published globally have confirmed how the growth outlook for the world economy in the latter part of 2023 and the first part of 2024 is worsening. This could lead analysts to revise downward their estimates of earnings performance in 2024, which, as is usual, seem to be too optimistic at the moment, making equity market valuations even more expensive, while reducing investors' appetite for risk," Perrotta further notes.

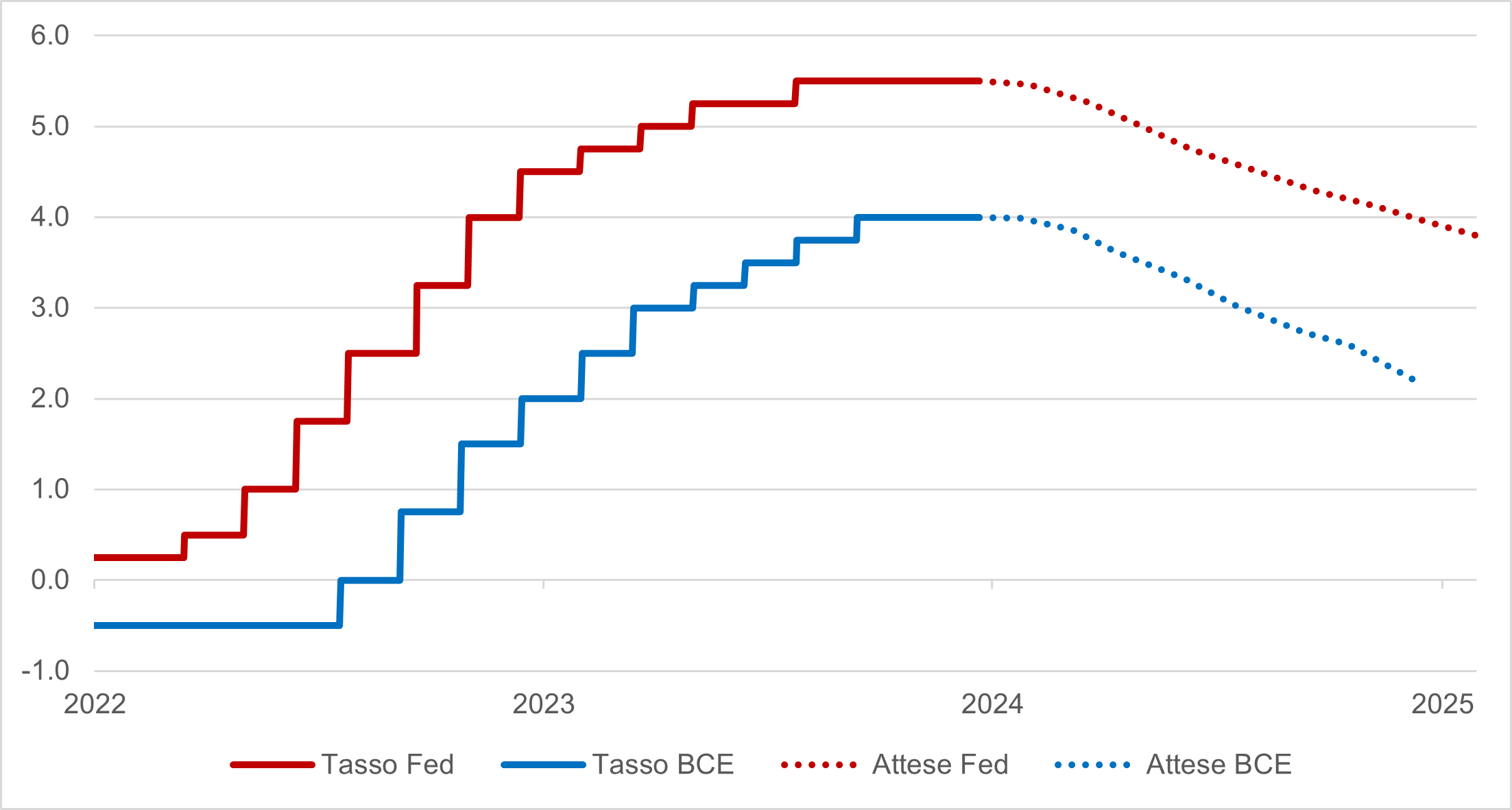

Expectations of a possible reversal of restrictive monetary policy by the Federal Reserve and the European Central Bank over the next year may only partially offset the negative impact of the economic slowdown, considering also that the response of central banks to the downturn may be slow due to continuing concerns about the inflation outlook.

"In such a scenario we lean toward a neutral positioning on global equities," he adds. There has been a significant polarization of performance during 2023, a consequence of the concentration of some markets in certain segments. Factoring in what has already been incorporated into prices, again, as much diversification as possible in terms of geography and sector is recommended.

"Finally, we recommend taking advantage of future phases of volatility to invest more profitably in both the bond and stock markets," the Head of Financial Advisoy continues.

Within a portfolio construction that is as diversified as possible, the geographic aspect is accompanied by a currency component, to be implemented on the equity and bond side according to various dynamics.

"This approach to portfolio management is in line with what was built and recommended in 2023, a year in which Banca Generali's clients were able to benefit from the significant returns achieved by the markets, thanks to the indication to remain invested, in the belief that the global recession expected by many did not represent the central scenario of the major international bodies and that there was therefore room for an upward revision of corporate earnings with a consequent positive impact on financial market prices," he concludes.

Generoso Perrotta, Head of Financial Advisory at Banca Generali

Generoso Perrotta, Head of Financial Advisory at Banca Generali