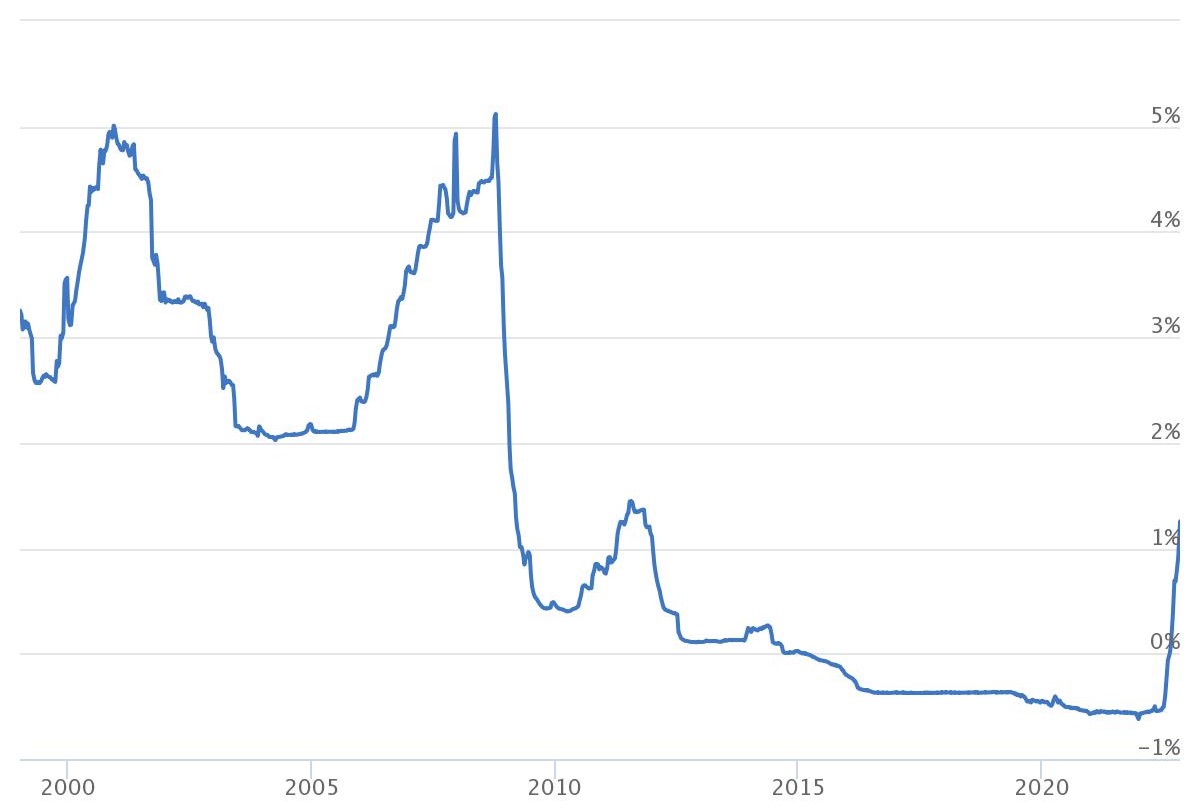

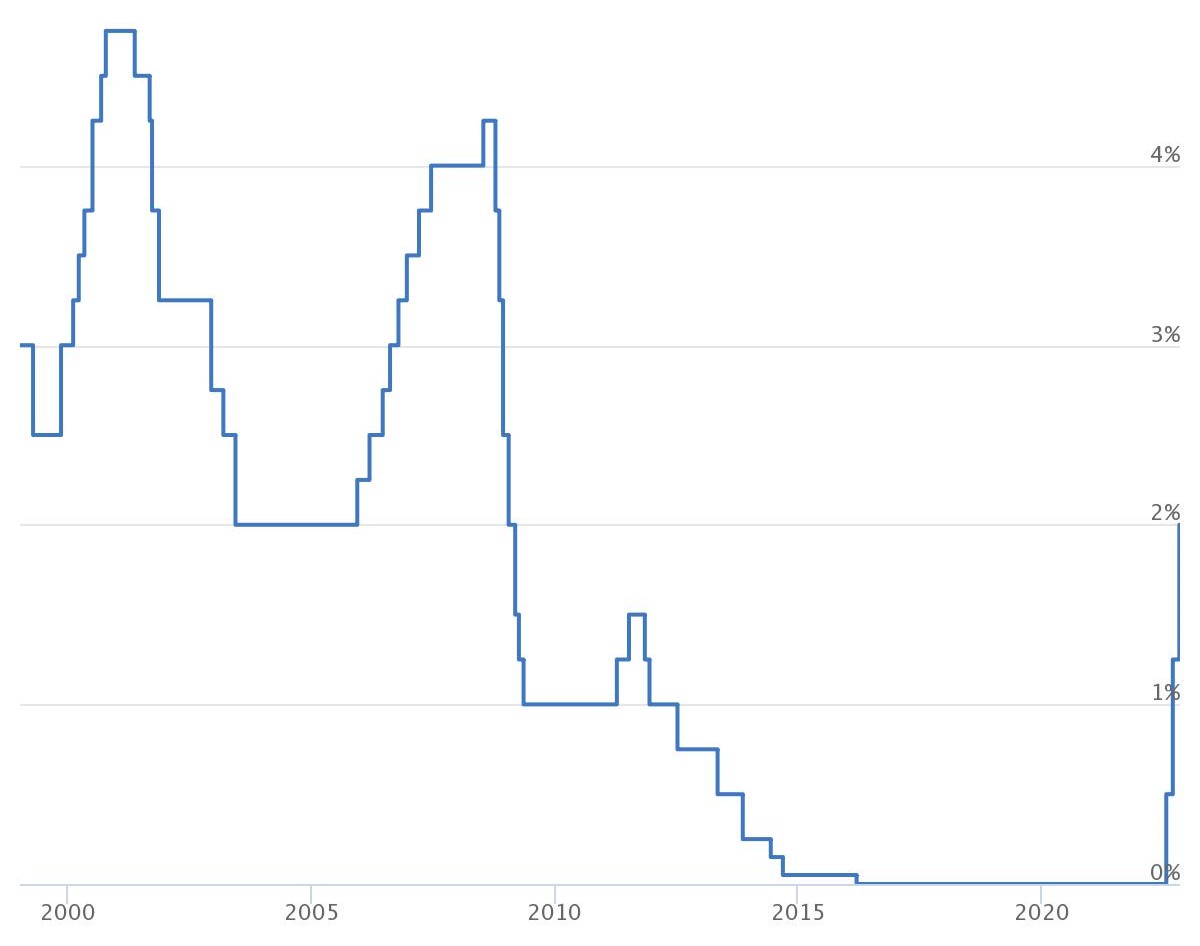

Through QEs, central banks put a lot of money into circulation by buying mainly debt securities in the market, especially bonds issued by states or even private companies. In certain historical periods, for example after the crisis of 2008 or the euro crisis of 2012-2013, where there was even a risk of ending up in a spiral of deflation, that is, a general decline in prices caused by economic depression, Quantitative Easing has been helpful in bringing about a reversal of the business cycle.

Under those historical circumstances, the conditions under which QE was decided were very different from those of today. In fact, back then there was very low inflation trending toward zero. Today, prices are rising at rates not seen in decades because of several factors: in America because of a consumption rush and a rise in wages, in Europe mainly because of commodity price increases caused by the war between Russia and Ukraine.

"Quantitative easing (QE) has been the main monetary policy tool over the past 10 years," explains Paolo Baldessari, head of Fixed Income & Alternative Investments at Banca Generali, who adds, "Central banks, grappling with the economic collapse that followed the Great Financial Crisis of 2008, understood that interest rate leverage was insufficient to effectively pursue their objectives."

However, Baldessari goes on to explain, "With inflation back in double digits, central banks have begun to move the traditional leverage of rates again, quickly pushing them into restrictive territory to 'cool' the economy and prices."

Paolo Baldessari, Head of Fixed Income & Alternative Investments at Banca Generali

Paolo Baldessari, Head of Fixed Income & Alternative Investments at Banca Generali

/original/BLOG+-+BANNER+%288%29.png)