Corrado Cominotto, head of active asset management at Banca Generali

Corrado Cominotto, head of active asset management at Banca Generali

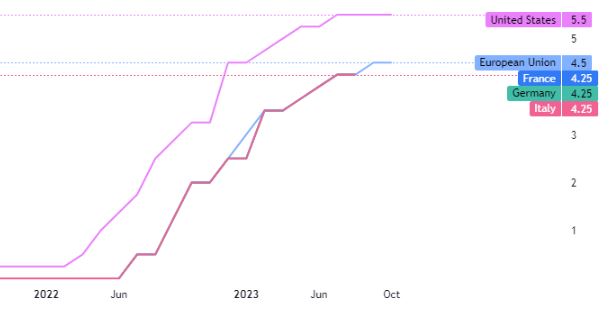

The market does not expect any more hikes, let alone for the December 14 summit. Instead, 30 percent of analysts assume a first rate cut in March 2024.

What is the economic outlook for the coming months and how far can the Fed and ECB interest rate axe go? To answer this question, we can start with one data point: a surprise number that has taken even economists by surprise but testifies to the resilience of the U.S. economy in the face of the season of hikes to stop inflation.

The 4.9 percent growth in U.S. GDP in the third quarter is the largest since the last quarter of 2021. The figure cannot but have also influenced the Fed's choice. Which for the second consecutive time left interest rates unchanged at 5.25-5.5 percent. Chairman Jerome Powell acknowledged that "persistent changes in financial conditions may have implications for the course of monetary policy," which is why financial developments are being "closely monitored."

Source: Trading View

Corrado Cominotto, head of Active Asset Management at Banca Generali, notes that "since July 27, the day after the Fed's last speech, the yield on the U.S. 10-year has risen from 4 to 4.8 percent, signaling how the rate curve is linked to the dynamics of yields." Then again, on July 31, the U.S. Treasury surprised the market by announcing the need to issue more debt than expected.

The U.S. government raised a net $1.007 trillion through the sale of bonds in the third quarter-the largest ever cash raise. The government bond market is largely driven by investors' expectations of a more resilient U.S. economy. There are now lower expectations of recession. As a result, investors are demanding a higher premium for holding longer-dated bonds.

However, it is not a given that we have reached the bullish peak by the Federal Reserve, quite the contrary. Two numbers must be read carefully: the U.S. unemployment figure and the inflation figure.

Cominotto points out how "in September the former was at 3.8 percent, a higher value than the low of 3.4 percent at the beginning of the year, while the inflation rate fluctuates between 3.4 percent of the Pce to 3.7 percent of the Cpi," the former relating to consumers' personal expenditures, the latter more detailed because the concerns consumer prices. Values far from the starting thresholds, between 7 and 9 percent. "For December and January, the Fed's next two meetings, 20 percent of analysts expect a possible rate hike, while they are expected to fall starting in the second quarter of 2024," Cominotto further explains.

In Europe, the scenario is completely different. "The market does not expect any more hikes, let alone for the December 14 summit. Instead, 30 percent of analysts assume a first rate cut in March 2024," the expert adds. On the other hand, growth estimates are completely different: according to JP Morgan, the EU GDP in 2023 stands at 0.7 percent while the U.S. GDP is expected at 2.5 percent. In the euro-dollar dynamic this partial misalignment is registered with a depreciation of the euro against the greenback. With the exchange rate moving from 1.12 to 1.06 euros from July to now.

Regarding macro scenarios, "the winds of war in the Middle East have not moved to the markets at the moment. It is not considered a possible escalation. There may be a flare-up in oil prices, although Brent is currently worth $88 per barrel, but on Sept. 27 it was traveling at a high of 96. On gas, on the other hand, volatility is impressive: from 150 euros per megawatt-hour Ttf in early December 2022 to lows of 26 euros in July to 50 today. The bullish trend can spill over to inflation in Europe as it affects bills," Cominotto explains.

Corrado Cominotto, head of active asset management at Banca Generali

The market does not expect any more hikes, let alone for the December 14 summit. Instead, 30 percent of analysts assume a first rate cut in March 2024.

/original/BLOG+-+BANNER+%288%29.png)