The OECD has calculated that under the assumption of a 20 percent reduction in energy input imports, the sectors in Europe that would suffer the most would be the most energy-related sectors, such as refineries and transport.

08 June 2022#WeeklyWatch

The Russia-Ukraine conflict and the commodity crisis

In the port of Odessa, on the shores of the Black Sea, a dramatic countdown has begun. Within about two weeks, ships loaded with export grain, which have been stuck at their berths since the war between Russia and Ukraine began, must necessarily leave and put out to sea, otherwise the material they are carrying will be irreparably doomed to rot.

This affair, which is discussed daily in the media almost all over the world, well represents the side effects on the commodities (in English commodity) market caused by the war wanted by Russian President, Wladimir Putin, which is longer than expected and still without a glimmer of a cease-fire.

Indeed, the Russian-Ukrainian conflict is one of the factors that has inflamed the already "red-hot" prices of commodities: not only those used as energy sources (oil and gas) but also industrial metals and agricultural products (wheat and corn) that feed many countries around the world. Even before the war, commodity prices had surged sharply, driven by the economic recovery following the Covid-19 pandemic. The conflict between Moscow and Kiev has since complicated matters, although an important point should be made: because financial markets live on expectations, the soaring commodity prices discussed in newspapers and on the news every day discount future scenarios and risks in advance.

In other words, while it is true that the "commodity" topic is much discussed in the press today, it is now somewhat less topical in the financial markets than it was at the time of the outbreak of war. That being said, it is good to know in detail how the war scenario has affected the markets.

War in Ukraine: why has it caused commodity prices to rise?

The effects of the war in Ukraine on the commodities sector, and consequently on GDP growth as well as inflation, were analyzed in detail by the OECD (the Organization for Economic Cooperation and Development) in its latest economic outlook, updated at the end of March.

The OECD data were also commented on by Massimo Taddei, economist at LaVoce.info, who highlighted some key points.

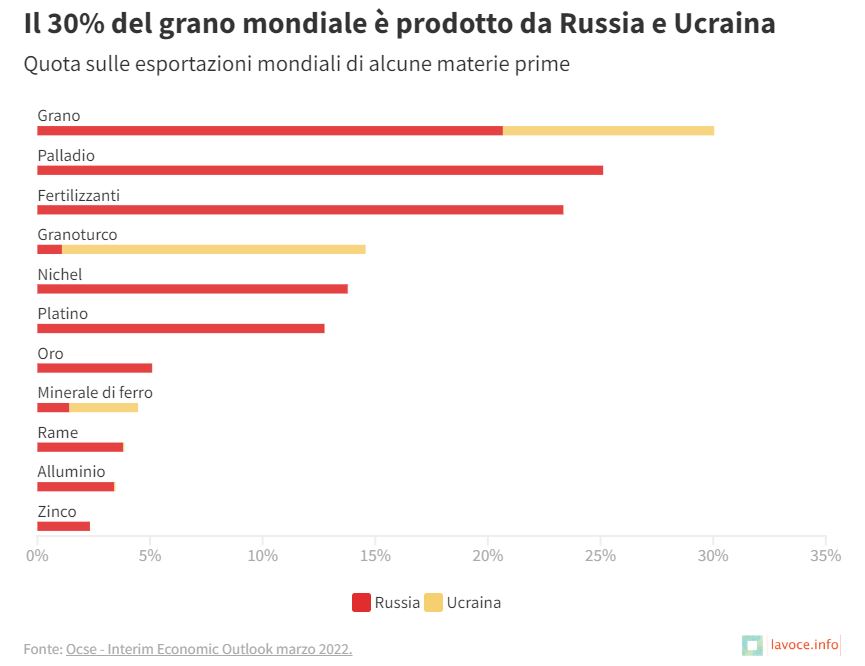

First, Taddei points out, "due to the extent of their territory, Russia and Ukraine are large producers of agricultural commodities. The two countries account for nearly one-third of the world's wheat exports and 15 percent of corn exports. Russia is also rich in natural resources. In addition to natural gas and oil, it boasts 25 percent of the world's palladium exports, 13 percent of nickel and platinum exports, and about 3 percent of aluminum and copper exports."

Given the importance of Russia and Ukraine in grain production, the war (and the West's embargo on many Russian products) could therefore theoretically lead to an increase in food prices around the world, particularly in the least developed countries. According to the OECD, in the event of a total paralysis of exports in Ukraine, the average increase in food prices could reach as high as 16 percent, putting several countries that import a lot of grain such as those in North Africa and the Sub-Saharan region in trouble.

Of course, this is a hypothetical scenario and there are many who think it will not happen, especially since there is progress in negotiations to unblock Ukrainian ports and get agricultural trade resumed. However, it is interesting to see how, on a theoretical level, events are chained together and the war has a potential impact on industry as well.

Fonte dati OCSE

Rising commodity prices and the effects on industry and GDP

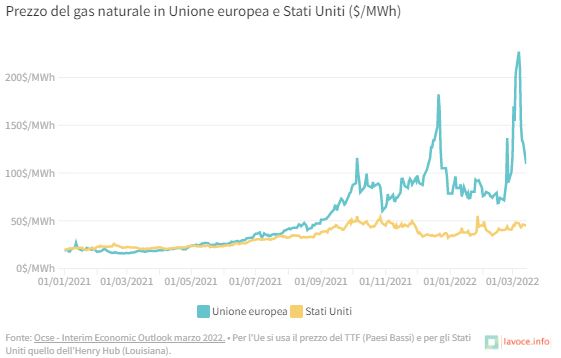

Indeed, it should not be forgotten that about 38 percent of the natural gas consumed annually in the Old Continent comes from Russia (data updated to 2020).

"The OECD," Taddei continues in Lavoce.info, "has calculated that under the assumption of a 20 percent reduction in energy input imports, the sectors in Europe that would suffer the most would be the most energy-related sectors, such as refineries and transport." Specifically, there are sectors such as pharmaceutical production, textiles or electronics where the potential drop in output is between 0 and 1 percent.

In other industries such as chemicals, metallurgy, and rubber-plastics, the potential decline in output is between 1 and 2 percent, while in air transport there is a risk of well over 2 percent. This is a completely hypothetical scenario but one that, if it reverified even partially, would cause a slowdown in economic growth worldwide.

Not surprisingly, according to the spring economic forecast prepared by the European Union, GDP growth in the Eurozone in 2022 could stop at 2.7 percent, one and a half points lower than previous estimates. In contrast, the U.S. economy is expected to grow by 2.9 percent (about 1.6 percent less than last months' estimates) although one thing should be highlighted: the U.S. is undoubtedly less exposed to the effects of the war, since it is less dependent on Russian raw materials. Indeed, the macroeconomic data published overseas during May confirmed the scenario of increased consumption and activity by U.S. businesses, against a background of persistent price pressures.

The effects on inflation, currencies, and employment

Beyond the differences in the effects on individual countries, one thing is certain: rising commodity prices have a potential domino effect on the world economy. Indeed, commodity shortages push up consumer prices, that is, inflation. To stem the rising cost of living, central banks then are pressured to raise interest rates, thus reducing the amount of liquid money in circulation.

But rising interest rates usually also cause a slowdown in consumption and the economy, and can have negative effects obviously on employment, which is always linked inseparably to gross domestic product dynamics.

Finally, currencies should not be forgotten. Usually, when central banks raise rates, there is also an appreciation of the domestic currency because international investors tend to buy financial assets in those countries that offer higher interest rates on their government debt securities.

This is what happened, for example, to the dollar, which appreciated against the euro in recent months as soon as the U.S. central bank (Federal Reserve) began raising interest rates, while the European Central Bank (ECB) remained in a wait-and-see position. Then, however, there was a rebalancing between the two currencies as there was a scaling back of rate hike expectations on both sides of the Atlantic.

Fonte dati OCSE

Private Banking: how to invest in commodities?

All events are precisely chained, while in the commodity market there is another player that should not be underestimated. This is China, which is both a major producer and consumer of commodities. After a sharp slowdown in industrial activity in recent months due to a resurgence of the Covid-19 outbreak, the latest commodity index in Chinese revealed improvements in both industrial production and market demand.

It is still too early to tell what direction Beijing's economy will take, but it will certainly play a decisive role in the commodity market as well. As we wait to see what scenario lies ahead, how should investors behave?

As already pointed out, financial markets usually play it forward, and current prices of many commodities already reflect the whole scenario just described as well as being very volatile. Therefore, it is not certain that there will be further price rises. However, if an investor wants to build a well-diversified portfolio with the help of a private banker, he or she can still reserve a space for commodities, which are now an important investment class (asset class).

But how does one go about investing in commodities? There are several financial instruments that allow you to bet on commodities. To choose the ones best suited to your needs, it is a good idea to rely on a good private banker. For those who want instruments that are not too complex, there are, for example, Etc's (Exchange Traded Commodities), which are financial products that can be traded every day on the stock exchange, whose value follows the changes in a reference index, specifically a basket of commodities.

For those who prefer to use an asset management tool, they can also choose an investment fund that specializes in the commodity sector. These are funds that have a portfolio composed of stocks of companies that extract, produce, and sell commodities, whose revenues and profits are obviously bound to rise if commodity prices rise.

Before taking action, however, it is best to consult with your trusted advisor since, even for commodities, the usual rule applies: it is better to devote a limited part of the portfolio to this asset class and to offset risks with other asset classes.

/original/BLOG+-+BANNER+%288%29.png)